How State Banking Rules Steer Funding Routes in Virtual Table Game Sessions Across Expanding US Markets

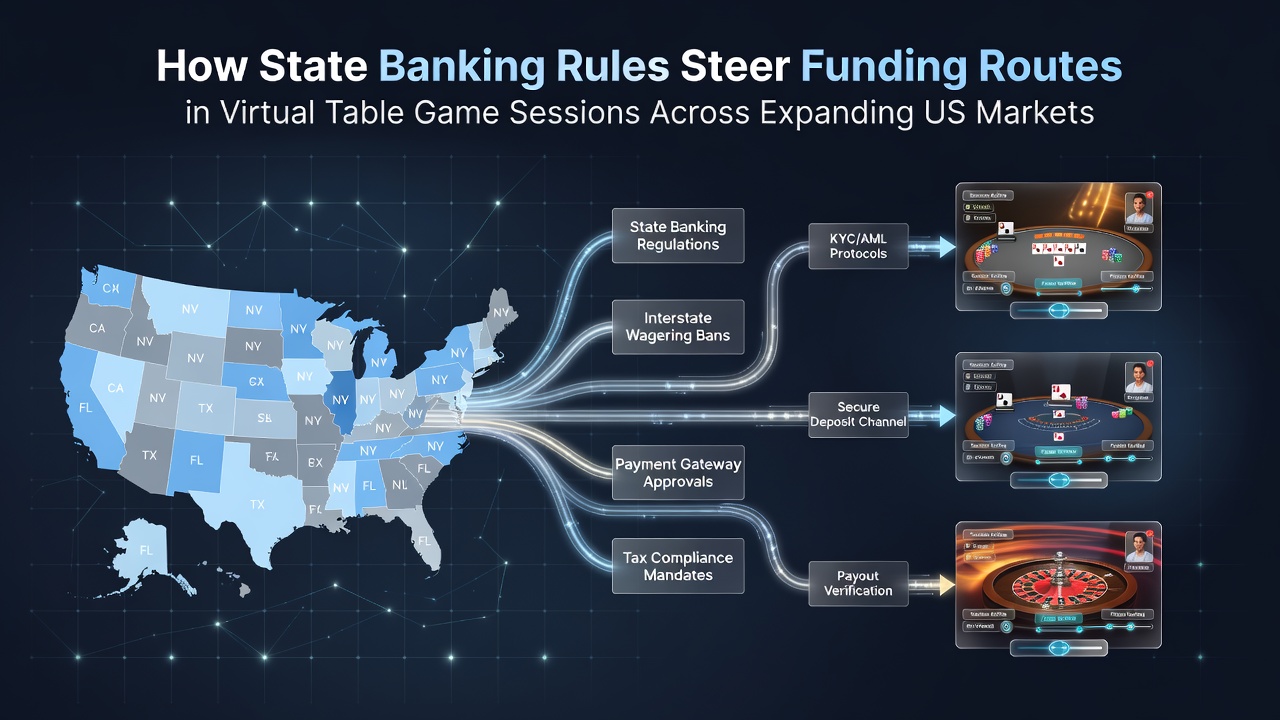

State banking regulations shape the pathways players use to fund virtual table game sessions in online environments across the United States, and these rules create distinct patterns in how deposits and withdrawals occur in newly authorized markets. Different jurisdictions impose varying restrictions on financial institutions and payment processors, which in turn guide operators toward approved methods such as ACH transfers, specific e-wallets, and prepaid card systems. Data from regulatory filings shows that these constraints influence session structures because players adapt their funding choices based on available options in each state.

Observers note that banking rules often stem from interpretations of federal laws like the Unlawful Internet Gambling Enforcement Act combined with state-level statutes, and this combination produces a patchwork where one state permits broader processor integrations while another limits activity to in-state banks. In practice those limitations steer traffic toward methods that comply with local oversight, and figures from transaction reports indicate higher reliance on wire-based systems in restrictive environments.

Regulatory Variations Across Jurisdictions

States that have expanded online table game access apply distinct banking frameworks, and these frameworks determine which processors can handle funds for blackjack, roulette, and poker variants. Pennsylvania and Michigan maintain systems that integrate with established financial networks, whereas newer entrants such as Ohio and New York introduce additional verification layers that affect routing speed and available channels. Research from state gaming reports reveals that operators adjust their platforms to match these requirements, and session data shows corresponding shifts in deposit timing and amounts.

By July 2026 several additional states had moved forward with virtual table game legalization, and the banking rules implemented in those markets followed patterns seen in earlier rollouts. Compliance teams at licensed platforms coordinate with regional banks to ensure funding routes remain operational, and this coordination reduces disruptions during peak playing hours. Analysts tracking payment trends have documented that states with stricter bank participation requirements see slower adoption of certain digital wallets compared with jurisdictions that allow more flexibility.

Impact on Funding Routes for Virtual Sessions

Banking rules directly affect the sequence players follow when loading funds into virtual table environments, and many jurisdictions require processors to maintain segregated accounts that meet state audits. This setup favors methods like direct bank transfers over credit card transactions in some regions, and transaction logs indicate that players in restrictive states complete funding steps through multi-step verification processes. Operators respond by highlighting compliant routes on their interfaces, and usage statistics demonstrate measurable differences in preferred channels between states.

Those who've examined payment processor integrations note that rules governing reserve requirements and anti-money laundering checks create bottlenecks for certain funding types, while approved alternatives maintain smoother flows. In expanding markets the emphasis on in-state financial partners leads platforms to prioritize ACH and wire options, and player behavior data collected by operators reflects longer intervals between deposits when alternative methods face delays. State regulators publish periodic summaries that outline these routing preferences without revealing individual account details.

Patterns in Emerging State Markets

Emerging markets introduce fresh banking stipulations that alter how virtual table game sessions are funded, and early data from these areas shows players gravitating toward methods already vetted by local banks. States entering the space often model their rules after established programs yet add unique compliance steps, and this layering produces distinct session rhythms tied to funding availability. Reports compiled by industry monitoring groups track these shifts through aggregated transaction volumes, and the numbers illustrate how rule variations correlate with route selection.

Take one regulatory filing from a Midwestern state that required all processors to partner with chartered banks inside its borders, and the result was increased use of electronic checks over instant-load options. Similar requirements in other jurisdictions have produced parallel outcomes, and researchers compiling cross-state comparisons have identified consistent patterns where banking limitations extend the time needed to initiate table game play. Operators adapt by offering guidance on compliant funding sequences, and usage metrics confirm that players follow those sequences in the majority of cases.

Conclusion

State banking rules continue to direct funding routes for virtual table game sessions as US markets expand, and the resulting patterns emerge from the interaction between local statutes and federal guidelines. Transaction records and regulatory summaries provide evidence of how these rules shape deposit methods and session timing across jurisdictions. Observers tracking ongoing developments note that new state entries maintain this dynamic through tailored compliance frameworks, and the data supports ongoing adjustments by operators and players alike.